-By Anonymous for Now – Certified Financial Planner – Backstop Financial

From time to time, clients I meet with often have questions about debt management and how to properly adjust their risk levels over time. Roughly 80% of American households have debt so this is obviously a topic that many Americans face around the U.S. Granted, a lot of this debt comes in the form of a mortgage (Which you will absolutely want to stick around for at the end), however the average American still has over $20k in non mortgage debt as well. Today what I will discuss is how you should view debt and a unique framework that I believe will change how you view debt forever and hopefully sparks change in your behavior surrounding it moving forward.

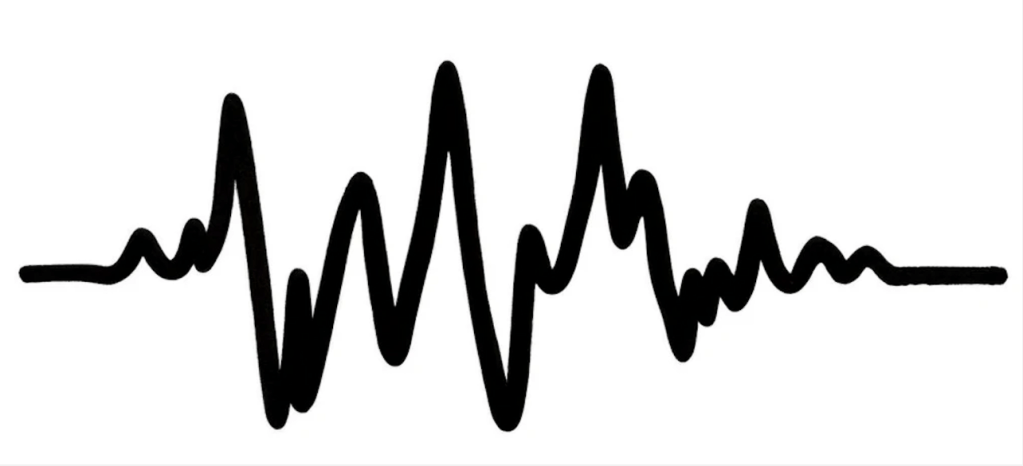

Take a look at this graph below:

These ups and downs are the obstacles that life can throw at you (Pandemics, Wars, disability, Divorce, gambling addiction, a delinquent child, death of your spouse, natural disasters, terrorist attacks, bad political descisions, job loss, etc.)… What I can unfortunately say without a shadow of a doubt is that you will absolutely face one of these at some point in your life – Hopefully not all of them! There is no way around this. And when it happens, it almost 100% guarantees that some level of financial burden will find its way in front of you. What debt does is decrease our tolerance to these events and puts us in a position to make desperate decisions such as having to sell real estate, stocks, take out a personal loan or something else that we would rather avoid if we had the option to do.

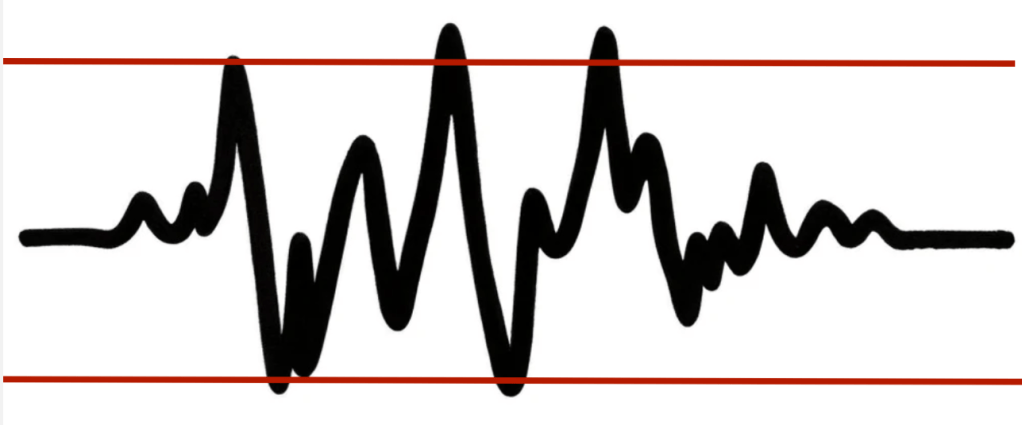

Now lets look at this same graph below and use the assumption that this is an individual who has very limited debt or no debt. Maybe they paid their house off, eliminated all consumer debts, and have a nice nest egg in retirement as well as an emergency fund. Their graph may look something like this:

The events are the same but their tolerance and ability to withstand these events, represented by the red lines, is very wide. In other words, outside of a few severe events, they are able to remain invested in the stock market, use cash to fund unpleasant surprises, and never experience an event that breaks them to the point where they begin to rapidly decrease wealth which can mean working for an additional decade or having to decrease your lifestyle…

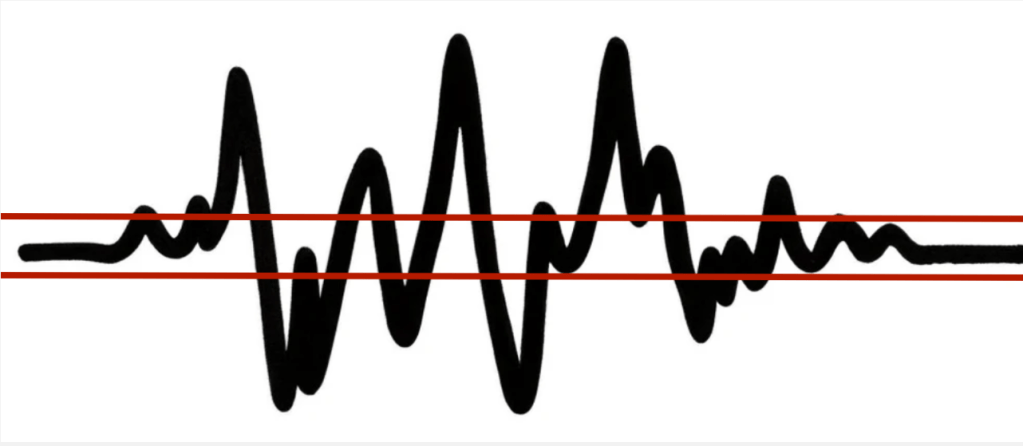

Let’s compare this to the average U.S. household who still has auto loans, student loans, credit card debts, a mortgage they are already struggling to afford, etc. What does this do to their tolerance of life’s curveballs?

It drastically shrinks their margin for error and peace of mind. Now when a pipe bursts and they have to pay out of pocket, they are already stretched so thin with other debt payments and no access to cash that they have to go further into debt which as you can guess, shrinks their ability to withstand future emergencies even further.

Now, how do we view this? What should our plan be for paying debt off and which debts should we feel comfortable hanging on to potentially? Should we go full Dave Ramsey and completely eradicate debt immediately? MAYBE – As a CFP I understand that paying off a 3% mortgage when you can make 8-12% in the stock market over time makes zero sense financially BUT it can make a massive difference PSYCHOLOGICALLY. If owning your house and having 12 months of cash reserves allows you to remain invested in the stock market when a crash happens because you have peace of mind to not panic sell, then you should absolutely do it. The psychological benefit at that point is exponentially larger than the 5-8% arbitrage we could earn annually for the time being. I work with clients who tell me that paying off their house in their 50s instead of waiting until their mortgage ran out at 60 is the greatest financial decision they have ever made and I can 100% understand why. I am in the process myself of paying down a 30yr mortgage and often dream of the day I own it outright (except for those pesky property taxes) /:

So what are some rules of thumbs? How should I view various debts? I’ll start with an easy one and go from there.

Credit Card Debts – Get rid of these before doing any other investing outside of your 401k Match. Why get your match first? It is likely a GUARANTEED 100% or 50% return on your money. You cant get that kind of return anywhere in the market place. Take the free money and then go knock out the credit card debt that is hanging out around 20%… If you can only earn 10-12% in the markets, having 20% interest build against you will be the death of you over time. KNOCK IT OUT NOW!

Auto Loans – In my firm we use a framework so you don’t get killed with interest – 25/3/10 – Put 25% down on the vehicle, finance for no more than 3 years, and the payments can be no more than 10% of your gross monthly income. Yes I prefer cash but also understand you need reliable transportation to your J.O.B. This rule keeps interest from accruing too quickly and leaves margin for you to invest, pay off credit card debt, and build cash if needed.

Student loans – We break these down by age as the older you get the less your expected rates of return can be in the market. If you are in your 20s and have student loan interest over 6%, pay off the debt first… For the 30s, if you are over 5%, pay off the debt first… And if you are in your 40s with student loan debt, pay it off no matter what. It has been hanging around your neck long enough. You are at the age where you want to begin to simplify your life and have less payments not more.

MORTGAGE – This is the one I have to arm wrestle clients on from time to time. Everyone wants to own their property and if they don’t they have just accepted they will never own it and decide to have a mortgage forever (No, we can do better than this). It is very unlikely if you are reading this and are a homeowner you have a mortgage over 8%. If you do, I believe that you should be paying off the mortgage as the premium investing in the markets adjusted with inflation simply isn’t worth it. Most of you probably find yourself in a range of 2% – 6% with either a 15yr or 30yr loan… Earlier I mentioned clients of ours view it as their best decision when paying off their mortgage earlier. They only get the green light to do this if the following are true: 3-6 month emergency fund, no other consumer debt, maxing out all tax advantaged retirement accounts, and their portfolio has grown to a size that if they stopped contributing they could still live the lifestyle they want to live and retire at the age they desire. The reason behind the last one is because we don’t want you having a paid off house and zero dollars working for you. The older you get, the less your dollars can work for you (see my previous blog post) which is why we cant support clients knocking out a mortgage without assets working behind the scenes. Once those rules are met, then and only then, do our clients get a green light to start pouring into the house at which point we support them 100%.

To conclude this, I would state the following. Stop viewing debt as a bridge that can get you to the things you desire with small payments. Instead, begin to view it as a dangerous tool that can narrow the amount of life’s obstacles you can comfortably withstand. Keep your margin of error as wide as you can and use debt only when you believe it to be absolutely necessary. Build cash for emergencies and buy as many assets as you can as fast as you can and reduce those liabilities.

Best of luck!

P.S. A few readers have asked for where they can review their own financial situation with myself. If you would like feel free to use this link –> One Page Financial Plan

-Anonymous for Now

Backstop Financial